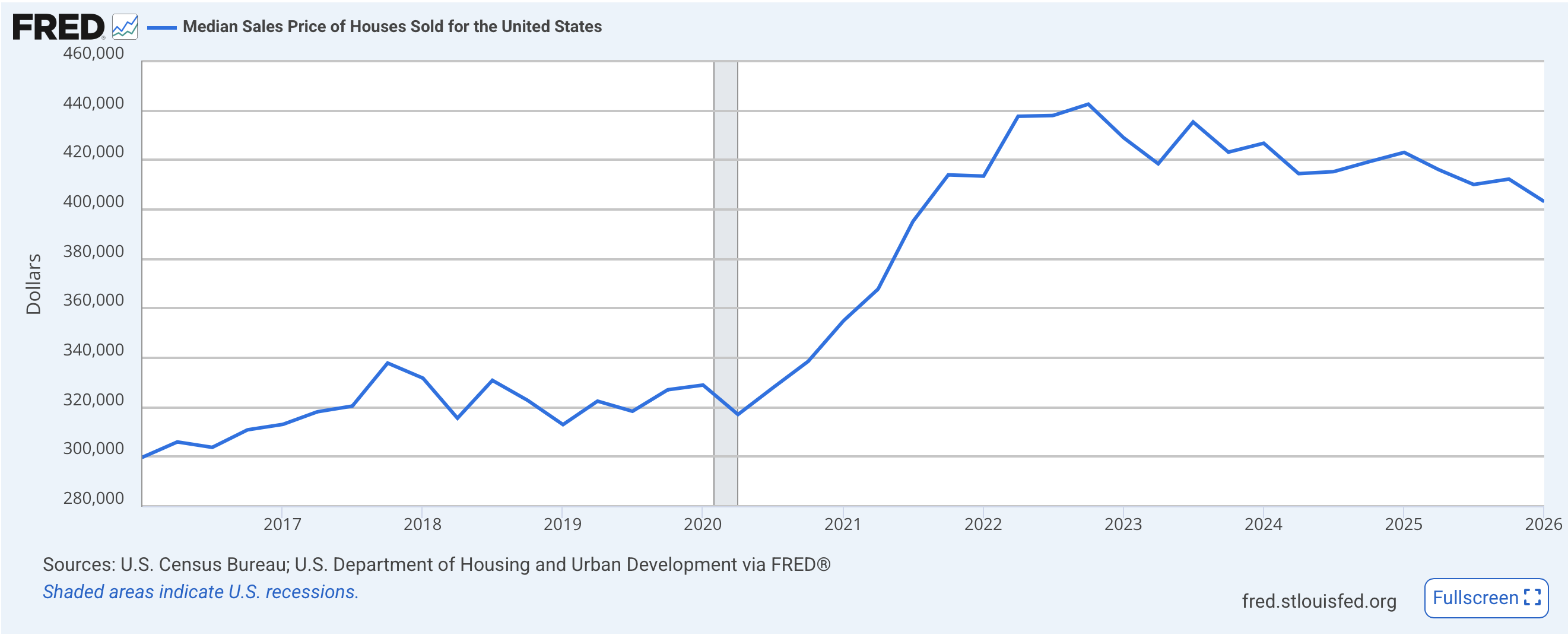

For over 25 years, I have analyzed housing and macroeconomic trends and how they shape real estate markets across New England. Following its peak in the fourth quarter of 2022, I expected the housing market to follow a more familiar correction pattern. As affordability spiked, prices would fall sharply, inventory would rise, and a traditional recovery cycle would begin. That did not happened.

Instead, the market has behaved asymmetrically and, at times, irrationally. Inventory shortages have helped to prop up values. National housing supply remains nearly 17% below typical pre-pandemic levels, with the Northeast still facing substantial inventory shortfalls.

Significant gains in equity markets preserved wealth at the upper end of the income spectrum. Psychologically, many sellers simply chose not to participate in the sell-off. Baby boomers and the silent generation have held onto large, high-value homes far longer than previous generations typically did. According to Redfin, nearly 40% of baby boomers who own homes say they never plan to sell.

The result has been a correction without the appearance of a true reset.

Source: Federal Reserve Bank of St. Louis, FRED

Source: Federal Reserve Bank of St. Louis, FRED

Movement Returns to the Market

I believe the correction is now largely behind us, but I would stop short of calling this a recovery. Prices in many markets have adjusted, expectations are becoming more realistic, and buyer activity is beginning to accelerate. We are starting to see something important return to the market: movement.

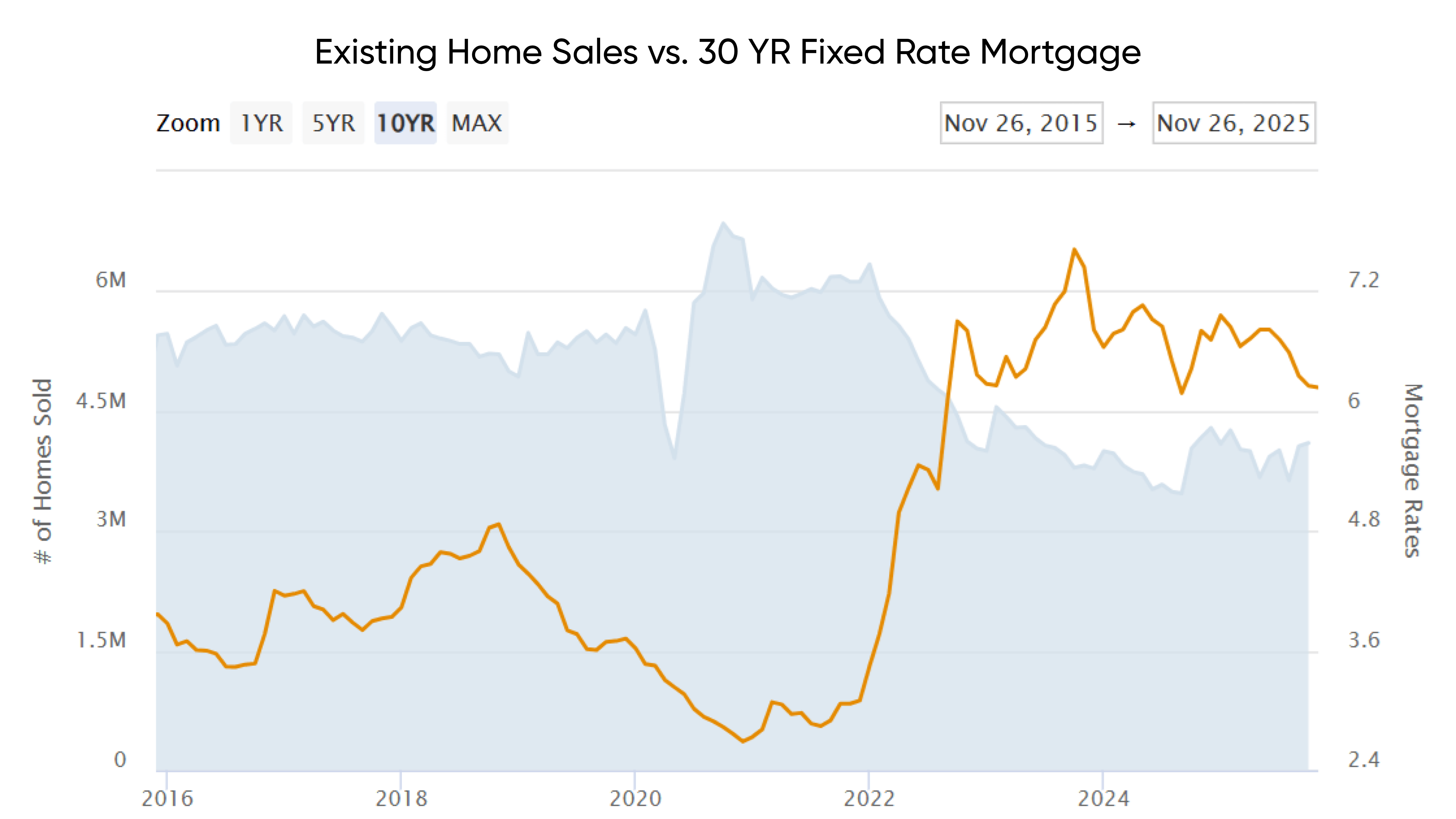

Two years ago, one of the key points I raised was the normalization of a 6% mortgage rate. Historically, the housing market can function at those levels. In October 2005, the average 30-year mortgage rate was roughly 6.25%. That same month, the seasonally adjusted annual existing home sale rate was over seven million units. Conversely, in October 2025, mortgage rates were at 6.2% but volume was stagnant at only 4.1 million units. The market has shown us it is capable of volume at these rates, it just needs to adapt.

Source: Federal Reserve | Department of Labor and Statistics

Capital is also beginning to shift. Money market rates are declining, investors are searching for alternatives, and real estate — particularly at the higher end — remains one of the few tangible asset classes with long-term durability.

A Slow and Uneven Recovery

That does not mean affordability pressures disappear overnight. The inflationary effects of the last several years will take a decade to fully work through the economy. Real wages are still catching up, and many middle-market buyers remain constrained. The recovery from here will likely be slow and uneven, similar to the years following 2009.

Luxury, however, continues to behave differently.

Quality and price point remain major differentiators, and in many markets, well-positioned luxury properties are continuing to hold value far better than the broader market. We are also beginning to see more inventory emerge as sellers slowly accept the new reality of the market. That thaw matters. Markets need movement in order to stabilize.

The Takeaway

Longer term, demographics will shape the next major chapter of housing. America’s largest generation (born 1990-2000) began entering their homebuying years around 2020, but affordability challenges and the COVID-era market frenzy delayed many purchases by several years. That demand wave likely extends through the early 2030s.

After that, the math changes.

Birth rates decline significantly beginning around 2001. In 1992, the US population increased by 3.5 million. By 2010, the rate had fallen by almost a third, to 2.5 million. In 2019, population increased by only 1.5 million. In 2024, the U.S. fertility rate fell to a record low of roughly 1.6 births per woman, which is well below the rate of 2.1, the pace necessary for equal replacement. Eventually, there will simply be fewer buyers available to absorb aging housing inventory. That reckoning is still years away, but it is coming.

The Opportunity Ahead

For now, though, the opportunity remains in front of us. The correction has created a more balanced and realistic market, even if it has not produced a clean recovery. Buyers are returning, inventory is improving, and the luxury market continues to demonstrate resilience.

In other words: The market is moving, so get on board.

About Joseph L. Taggart

Joseph L. Taggart is President & CEO of LandVest, where he has spent more than two decades helping shape the firm’s growth and strategic direction. He regularly shares quarterly commentary on the economy, housing market trends, and the broader forces influencing real estate across New England. Internally, he’s earned the unofficial title of LandVest’s “Chief Economist.”

More Posts by Joseph L. Taggart:

The Risk of Waiting to Sell: The Next Five Years in Today’s Market

The Existential Threat of the Bimodal Economy

Our Economy Has A Self-Esteem Problem

To landvest.com

To landvest.com

.jpg)

Follow Us on Social Media