The New England Luxury Real Estate Report is an annual review of select high-end markets in Maine, Massachusetts, New Hampshire, Rhode Island, Vermont, and the Adirondacks. Commentary and insights are provided by Luxury Real Estate Advisor Stewart Young of Cape Cod, Slater Anderson, Managing Director of Real Estate, and more than 75 residential real estate brokers, appraisers, and consultants. Market data is collected from Multiple Listing Services and do not include private listings and sales. In this report, we define “luxury real estate” as residential properties that sold in excess of $1 million to $2 million depending on the market.

While the current conflict in the Middle East has triggered economic uncertainty, this report reflects market activity in 2025 and the 19 years proceeding, during which time there have been multiple systemic shocks similar to the current events.

Overall New England Market Trends for 2025

Strong stock market performance continued to support demand for luxury properties.

In 2025, the high-end markets across New England and the Adirondacks continued a strong rebound in sales compared to the post-COVID slowdown of 2022–2023. Most of the markets making up the New England Luxury Real Estate Report — 24 of 35 — recorded increases in sales. Inventories improved throughout 2025, but in many markets demand still outpaced supply. While this remained a seller’s market overall, conditions began shifting toward greater balance in some northern markets. The strength of the stock market, combined with resilience in the Northeast’s technology, biotech, and financial sectors, continued to support the luxury segment despite elevated interest rates and broader economic and political uncertainty.

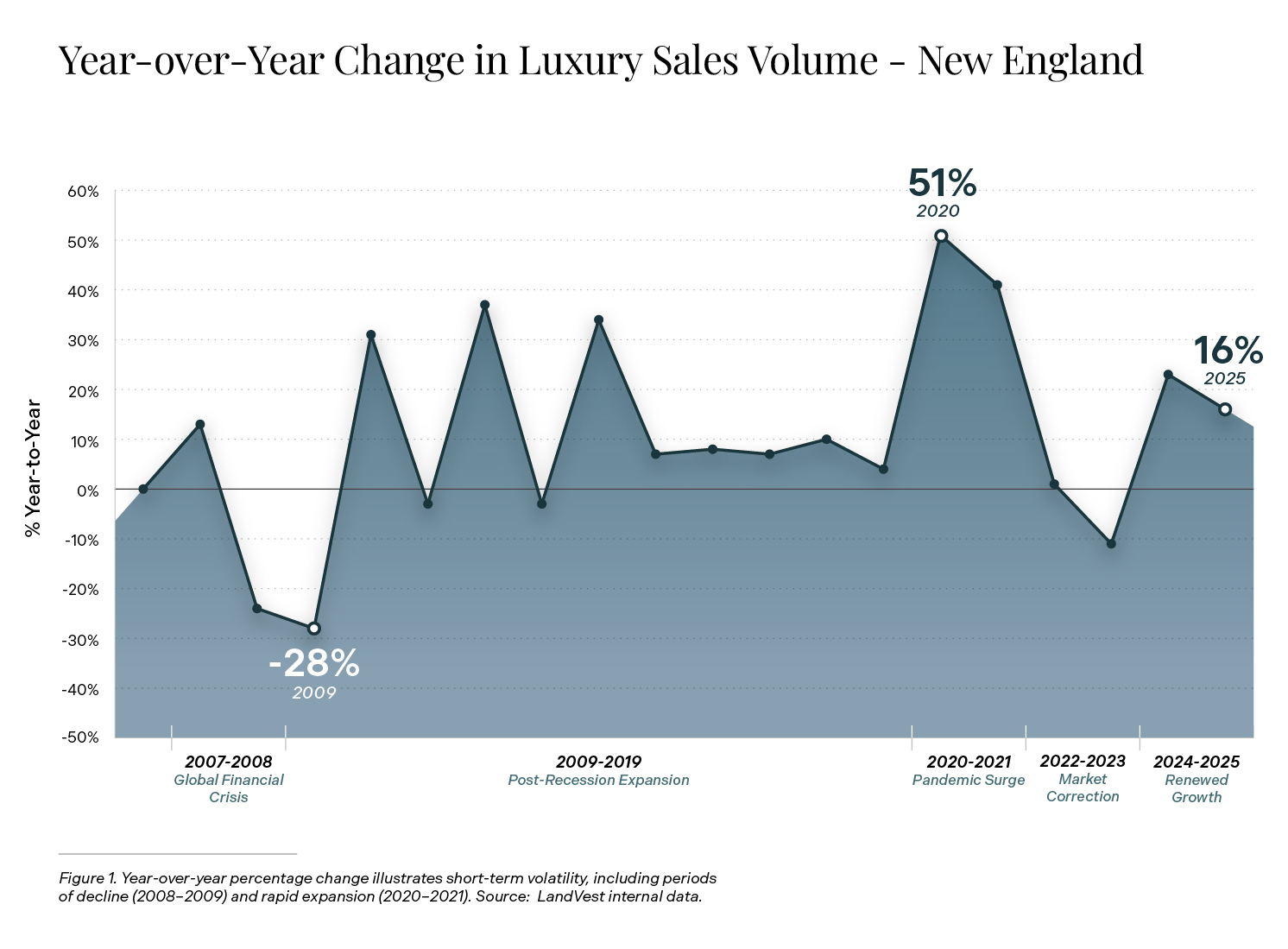

High-end luxury property sales increased by 16%

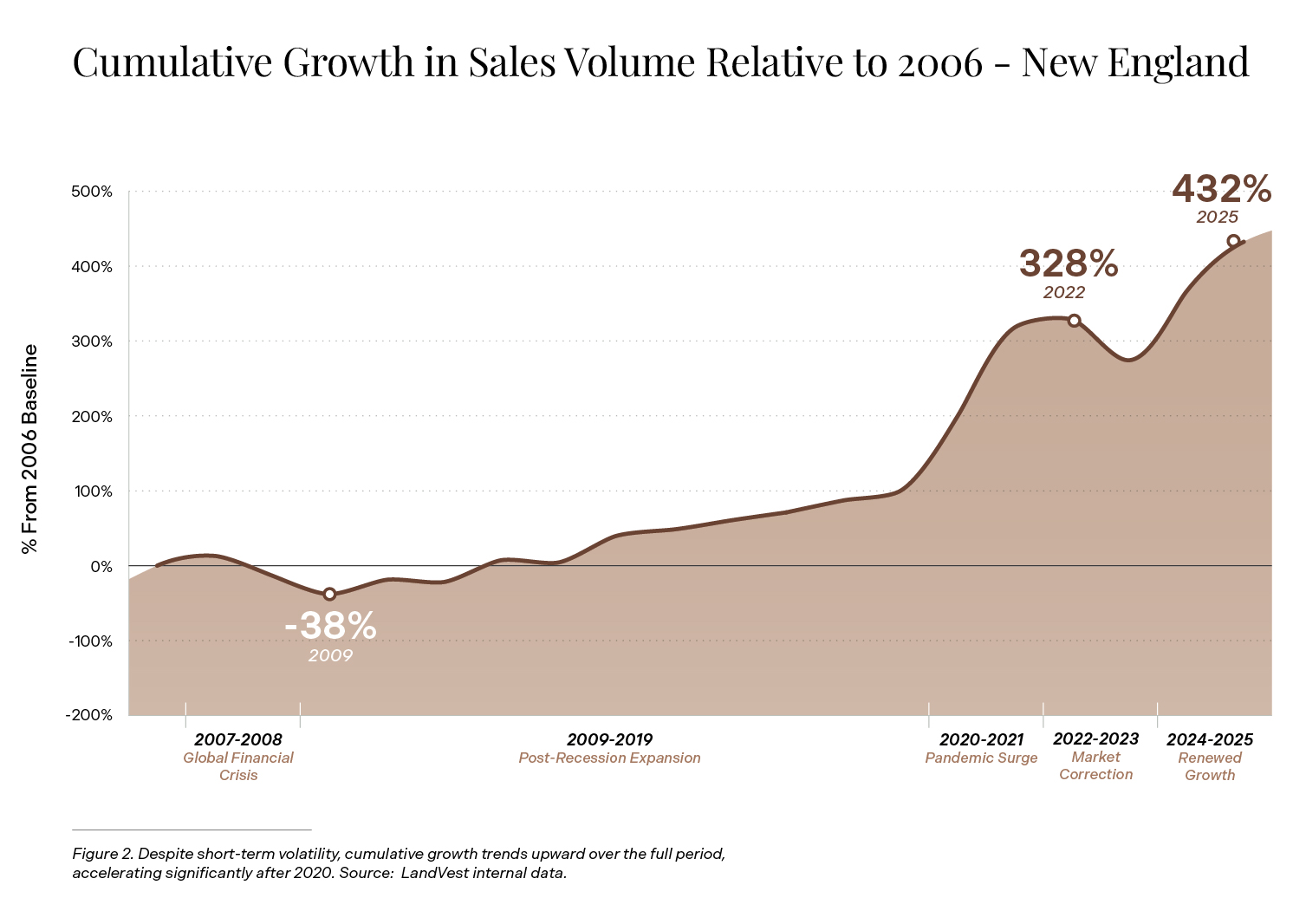

In 2025, luxury sales volume increased by 16% compared to 2024 (4,579 vs. 3,948 sales). For context, this represents the seventh-highest annual growth rate in the past 19 years. By comparison, the COVID years produced extraordinary surges in sales: +51% in 2020 and +41% in 2021. Compared to our baseline year in 2006 (861 luxury sales), 2025 sales are up 432%.

“High-end properties in the $2 to $3 million price range are experiencing bidding wars resulting in premiums for sellers, but at the highest end of the market, buyers continue to be selective, value conscious, and push back against overly aggressive pricing,” reports Stewart Young of the Cape Cod office.

New England 2025 Performance by State

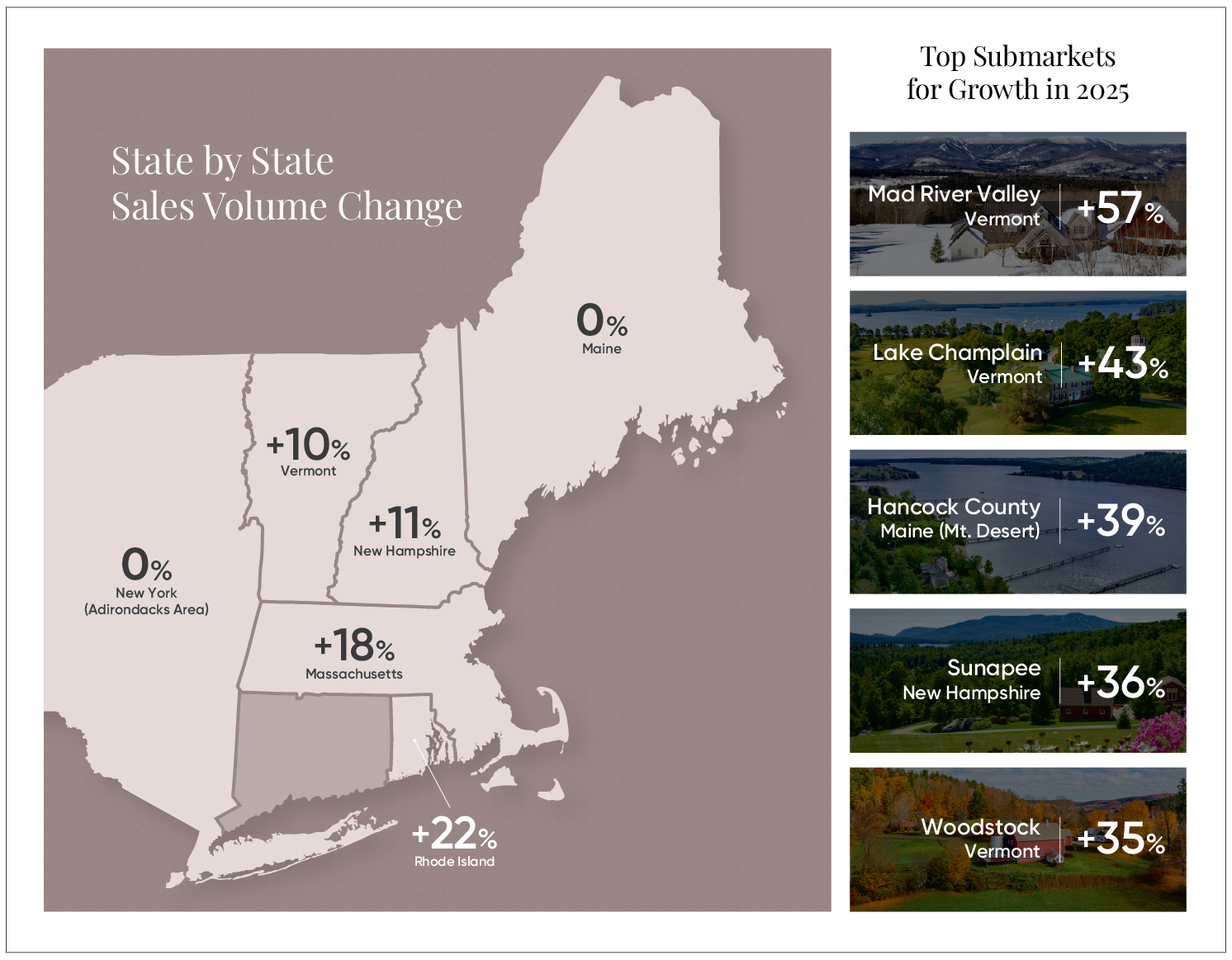

Four of the six states included in this report posted growth in high-end sales, while two were flat. By state, year-over-year luxury sales changed as follows: Maine: 0%, Massachusetts: +18%, New Hampshire: +11%, New York (Adirondacks): 0%, Rhode Island: +22%, Vermont: +10%.

Source: 2025 Sales volume change from 2024 by state. Source: MLS data.

Taken together, the regional story is not one of broad-based weakness or excess supply. Instead, 2025 was shaped by improving inventory, still-limited best-in-class offerings, and highly selective buyers. In many luxury markets, especially waterfront and village-centered destinations, activity remained healthy because affluent buyers continued to compete for scarce, turnkey properties even as they became more disciplined on pricing and condition. State and local Realtor data across New England also show a common pattern: inventory improved from historically low levels, but remained below what would be considered a balanced market in most places.

The top submarkets for growth in 2025 were led by Mad River Valley, Vermont (+57%), Nantucket (+50%), Lake Champlain, Vermont (+43%), and Hancock County, Maine and Bristol County, Massachusetts (each +39%). Markets with year-over-year declines included Merrimack/Monadnock, New Hampshire (-13%), Midcoast Maine (-6%), and the Berkshires / West-Central Massachusetts (-4%).

Massachusetts: Depth, wealth creation, and continued demand in marquee markets

In Massachusetts, buyers buoyed by strong financial markets and entrepreneurial wealth creation remained active, while sellers — especially downsizing baby boomers — were more willing to come to market. That combination helped push both inventory and transaction volume higher in many luxury submarkets. Statewide data showed sales and prices both moving higher in 2025, with single-family sales up and median prices continuing to rise. In Greater Boston, inventory gains also created a more functional market, even if well-located, high-quality homes still traded quickly.

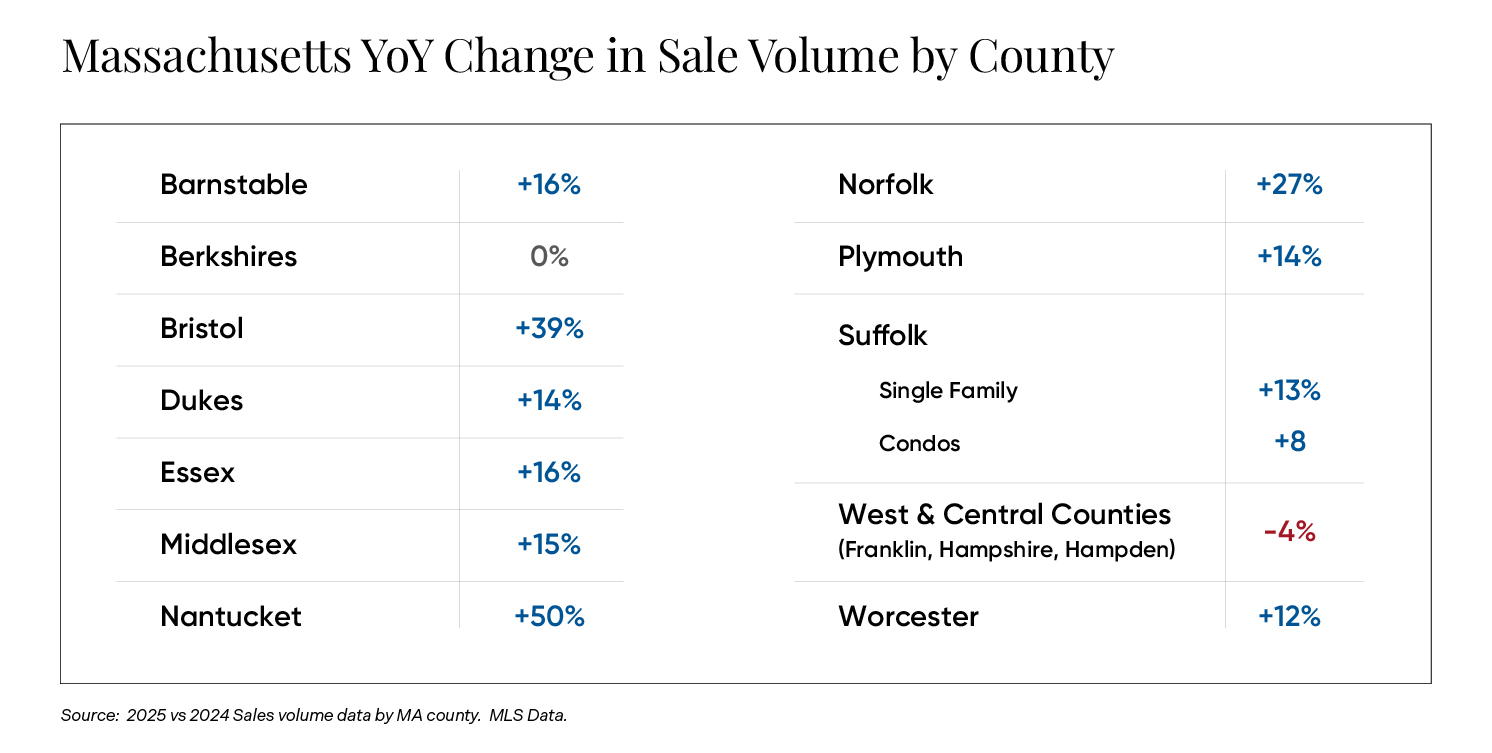

Sales were up in 11 of 13 Massachusetts markets in 2025, compared with decreases in all 13 markets in 2023. The three markets with the largest increases were Nantucket (+50%), Bristol County (+39%), and Norfolk County (+27%). The markets without gains were the Berkshires (0%) and West & Central Massachusetts (-4%).

The three largest vacation markets in Massachusetts continued to expand their luxury sales volume. Cape Cod increased 16% to a record 305 sales, above last year’s record of 264. Martha’s Vineyard grew 14% to 114 sales, still below the 2021 COVID peak of 161. After a 2% decline last year, Nantucket rose 50% to 310 sales, though still below the 2021 peak of 392. LandVest’s Martha’s Vineyard team also brokered an island-record $37.5 million sale for the Gatsby-inspired 48 Witchwood Lane.

Across Massachusetts — and especially in coastal markets — demand remained strongest for scarce, turnkey properties with prime locations and minimal renovation needs. That aligns with broader statewide data showing rising listings but still-constrained supply relative to demand, particularly in the highest-quality segments.

“The North Shore market remains very tight with pricing holding strong. Interest rates need to come down into the 5’s to generate more activity. Sellers can’t sell if they don’t have a desirable place to relocate to,” reports Lanse Robb, Broker in Manchester-by-the-Sea.

Maine: Flat transaction volume, but enduring scarcity in top coastal enclaves

While Maine’s luxury sales volume was flat in this report, the underlying market remained firm. Statewide Maine data for 2025 showed home sales rising and prices increasing year over year, with Maine MLS repeatedly pointing to improving but still limited inventory and steady buyer demand. That backdrop helps explain why prime coastal and lakefront luxury markets continued to command attention even when overall high-end transaction counts did not accelerate.

In practical terms, Maine’s luxury market continues to reward location specificity. Buyers tend to be highly focused on a short list of established destinations — places such as Camden, Boothbay, Mount Desert, Cape Elizabeth, York Harbor, and Prout’s Neck — which means that even modest increases in inventory do not necessarily soften pricing in the most recognized enclaves. Instead, additional supply often broadens choice while preserving competition for the best properties. That dynamic is consistent with statewide Maine data showing more homes coming to market without a sharp correction in values.

John Scribner, who services a wide swath of Maine from Coast to Lakes, reports: “We continue to see strong record sales activity. Buyers see the market softening based on world events, but sellers don’t believe that matters too much. Demand for communities with limited historic supply remains high. Folks that want Prout’s Neck will only take Prout’s Neck. Folks that want Camden will only take Camden. Folks that want Boothbay will only take Boothbay. This year it will be tougher for buyers to find what they want in the more known enclaves and buyers will need to expand their horizons.”

New Hampshire: Low inventory still defines the market

The defining New Hampshire theme in 2025 remained the lack of homes for sale. That is not just anecdotal: New Hampshire MLS reported inventory well below balanced-market norms throughout 2025, often in the 1.4 to 2.1 months of supply range. Even where inventory improved meaningfully year over year, it remained far below the 5–7 months typically associated with a balanced market.

The defining New Hampshire theme in 2025 remained the lack of homes for sale. That is not just anecdotal: New Hampshire MLS reported inventory well below balanced-market norms throughout 2025, often in the 1.4 to 2.1 months of supply range. Even where inventory improved meaningfully year over year, it remained far below the 5–7 months typically associated with a balanced market.

That helps explain why luxury demand remained resilient in the state’s lakefront and lifestyle-driven markets. Buyers had more choices than during the most constrained pandemic-era period, but not enough to weaken pricing for highly desirable properties.

According to Kristen Claire, who works across New Hampshire: “The last time New Hampshire saw a balanced market (5–7 months’ supply) was 2016, when statewide there were 7,300 single-family homes for sale compared to 1,434 coming into January 2026.”

That long-running supply shortage continues to support values in the upper tiers of the market, especially for waterfront and move-in-ready homes.

Rhode Island: Small-state scarcity continues to lift the top end

Rhode Island posted the strongest state-level gain in this report, with luxury sales up 22% year over year. That outperformance fits with broader statewide housing data showing a market that remained undersupplied even as the number of homes for sale began to improve. Throughout 2025, the RIMLS reported rising inventory, but also emphasized that supply remained too low to fully satisfy demand, keeping prices elevated.

For the luxury segment, Rhode Island’s appeal is straightforward: the state offers a concentrated set of highly desirable coastal communities, a relatively short distance to major Northeast wealth and cultural centers, and a limited supply of truly premium inventory. As a result, even incremental improvements in supply have tended to normalize market pace rather than undermine pricing. That has been especially true for well-positioned coastal properties, where scarcity still matters more than transient headlines like high mortgage rates or broader economic headwinds.

Vermont: Three of the five fastest-growing submarkets underscore the state’s momentum

Three of the top five non-Massachusetts submarkets in the report were in Vermont, led by Mad River Valley (+57%), Lake Champlain (+43%), and Woodstock (+35%). That concentration is significant. It suggests Vermont’s luxury gains were not limited to one isolated pocket, but reflected broader demand across multiple lifestyle-oriented markets.

MLS data also support the idea of a market that was becoming more functional without losing depth: prices, new listings, and active inventory all rose year over year in 2025. That points to a healthier flow of product rather than a drop-off in interest. For affluent buyers coming from higher-cost markets in the Northeast, South, and West, Vermont continued to offer a compelling combination of landscape, recreation, architectural character, and relative value.

The state’s luxury market also appears to be broadening in buyer profile. Rather than being driven solely by pandemic-era relocations, Vermont is increasingly attracting discretionary purchasers looking for four-season lifestyle, privacy, and quality of place. That shift makes the market feel more durable and less dependent on one-off migration waves.

Wade Weathers, Regional Manager for Vermont, reports: “The Burlington and Lake Champlain markets suffered from a lack of inventory, while the Stowe luxury market became more balanced, with increased inventory giving buyers more choice and more leverage. The Woodstock inventory is easing up slightly with a more balanced market for 2026.”

New York (Adirondacks): Permanently constrained supply supports long-term values

The Adirondack market is distinct. It is shaped by a finite supply of quality property and by land use protections that preserve the Park’s open-space character. The Adirondack Park Agency notes that the Park contains a large mix of public and private land, with the land use plan applying to roughly 2.9 million acres of private land and directing development in ways intended to conserve natural resources and minimize sprawl. That structural constraint helps explain why year-over-year transaction swings are often muted, while pricing for quality assets remains well-supported.

So while the Adirondacks were flat in sales volume in this report, flat does not mean weak. In a market with limited inventory and significant barriers to large-scale new supply, steady sales often reflect enduring demand meeting a naturally constrained pipeline. That dynamic continues to favor distinctive waterfront, mountain-view, and legacy-estate offerings.

As Matt Smith reports: “There are still more buyers than high-end listings, which has buoyed luxury sales in our region. As long as this supply-demand imbalance remains, quality listings can expect to rise in price.”

Looking Ahead to 2026

Geopolitical uncertainty, rather than underlying financials, may constrain market participants who are otherwise poised to continue stimulating growth.

The theme heading into 2026 is a gradual move toward a more balanced market, not a reversal. Inventory has improved across many parts of New England, but in most luxury segments it still has not fully normalized. That means sellers no longer hold quite the same degree of leverage they did at the height of the pandemic-era surge, yet truly exceptional properties remain in short supply.

“If mortgage rates can get below 6% in 2026, as we had hoped in 2025, then many sellers who were reluctant to part with their sub-3% mortgages may now be willing to move,” said Slater Anderson, Managing Director at LandVest | Christie’s International Real Estate. “We are also seeing the first signs in several years of speculative developers and builders looking to enter the market again. However, recent geopolitical events may increase cautiousness and put downward pressure on homebuilder sentiment in the near term as inflationary fears return.”

At higher price points, cash buyers continue to dominate sales and remain less sensitive to elevated mortgage rates. As a result, the New England luxury real estate market appears positioned for continued steady sales activity in 2026, with pricing likely to remain firm for best-in-class assets even as buyers become more selective.

About Stewart Young

Stewart Young is a LandVest | Christie’s International Real Estate agent and advisor focusing on Cape Cod, the South Coast, and Boston’s western suburbs. He compiles the New England Luxury Real Estate Report, which tracks sales of high-end properties across New England and the Adirondacks. In this report, luxury real estate is defined by market-specific thresholds of $1,000,000, $1,500,000, or $2,000,000, depending on geography.

About Slater Anderson

Slater Anderson is Managing Director at LandVest | Christie’s International Real Estate and contributes strategic market perspective to the annual New England Luxury Real Estate Report. Slater Anderson is also Managing DIrector of LandVest Consulting and has been a Certified General Appraiser since 2007 working across New England and nationally on complex and highvalue appraisal and consulting assignments. He has also participated in sales of over $265M in land and luxury residential properties over his 26 years at LandVest.

To landvest.com

To landvest.com

.jpg)

Follow Us on Social Media