Every historic home has a story. Some were shaped by influential families, others welcomed notable guests, and a few have been carefully preserved using the same techniques that built them centuries ago.

Stewart Young, a LandVest | Christie's International Real Estate Principal focusing on Cape Cod, the South Coast, and Boston's western suburbs, compiles the LandVest Index, which tracks sales of high-end properties across New England and the Adirondacks.

According to Young, In 2023 the high-end markets across New England and the Adirondacks retracted compared to the peak last year but continued to perform strongly on a historic basis. Wealthy millennials are driving the market for primary homes in the key suburbs and for second primary homes and vacation homes. On the downside, low inventories, negative economic factors, despite the strong stock market, and diminishing COVID driven demand continue to be important factors in the market. While high-end buyers tend to be cash buyers, our analysis suggests that they have reacted negatively to high interest rates as have buyers requiring financing.

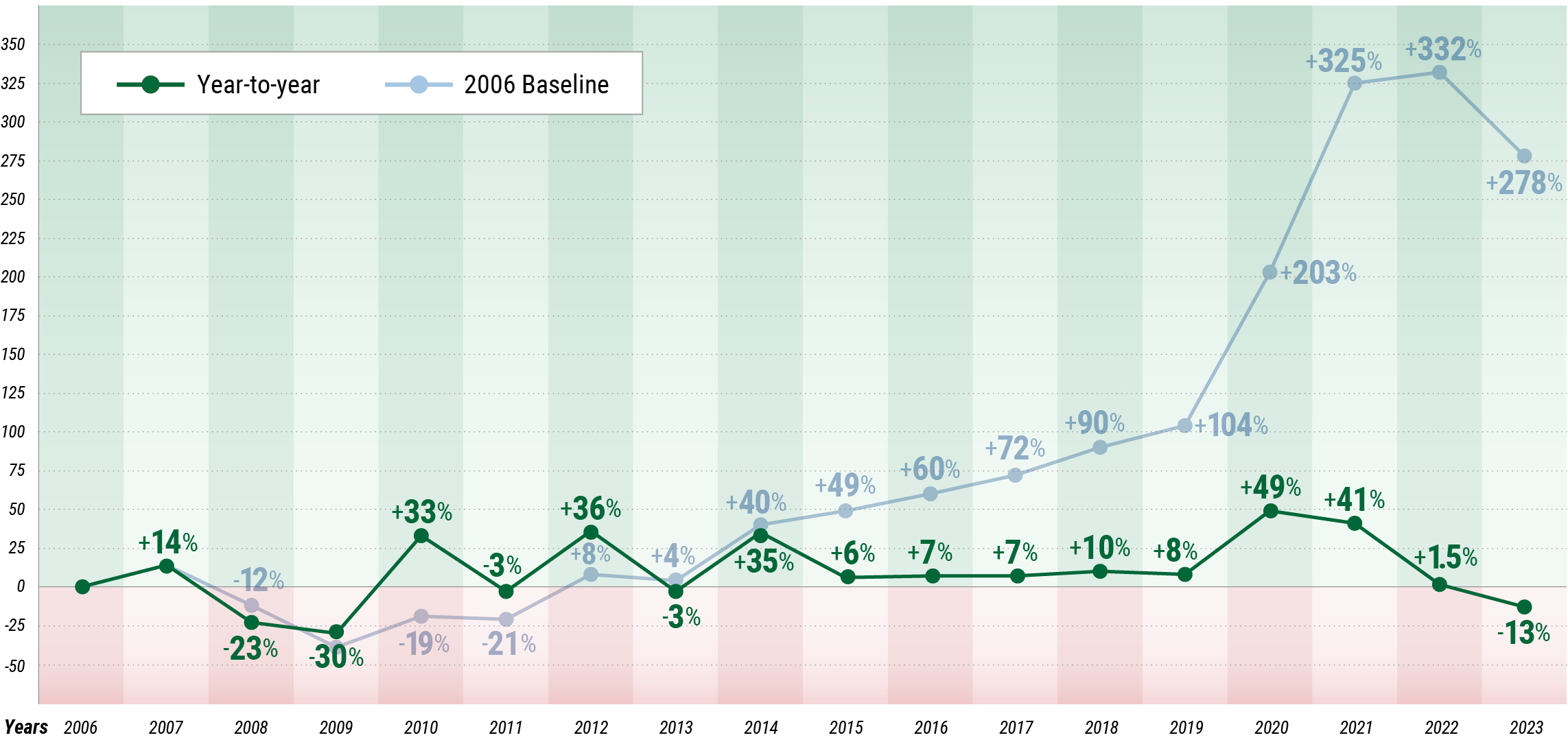

High-End Sales Volume - % Change Year to Year and Baseline 2006 Comparison

This years high-end sales volume decreased by 13% compared to 2022 (3,168 vs 3,622 sales). In contrast the COVID years had significant growth in sales: 49% in 2020 and 41% in 2021. Sales in 2022 slowed considerably but still showed growth of 1.5%. Compared to our baseline year in 2006 (838 sales), sales are up 278% vs 332% in 2022, and have recovered substantially from a bottom of 513 sales in 2009. High-end properties in the $2-3 million price range are experiencing bidding wars resulting in premiums for sellers, but at the highest end of the market, buyers continue to be selective, value conscious, and push back against overly aggressive pricing.

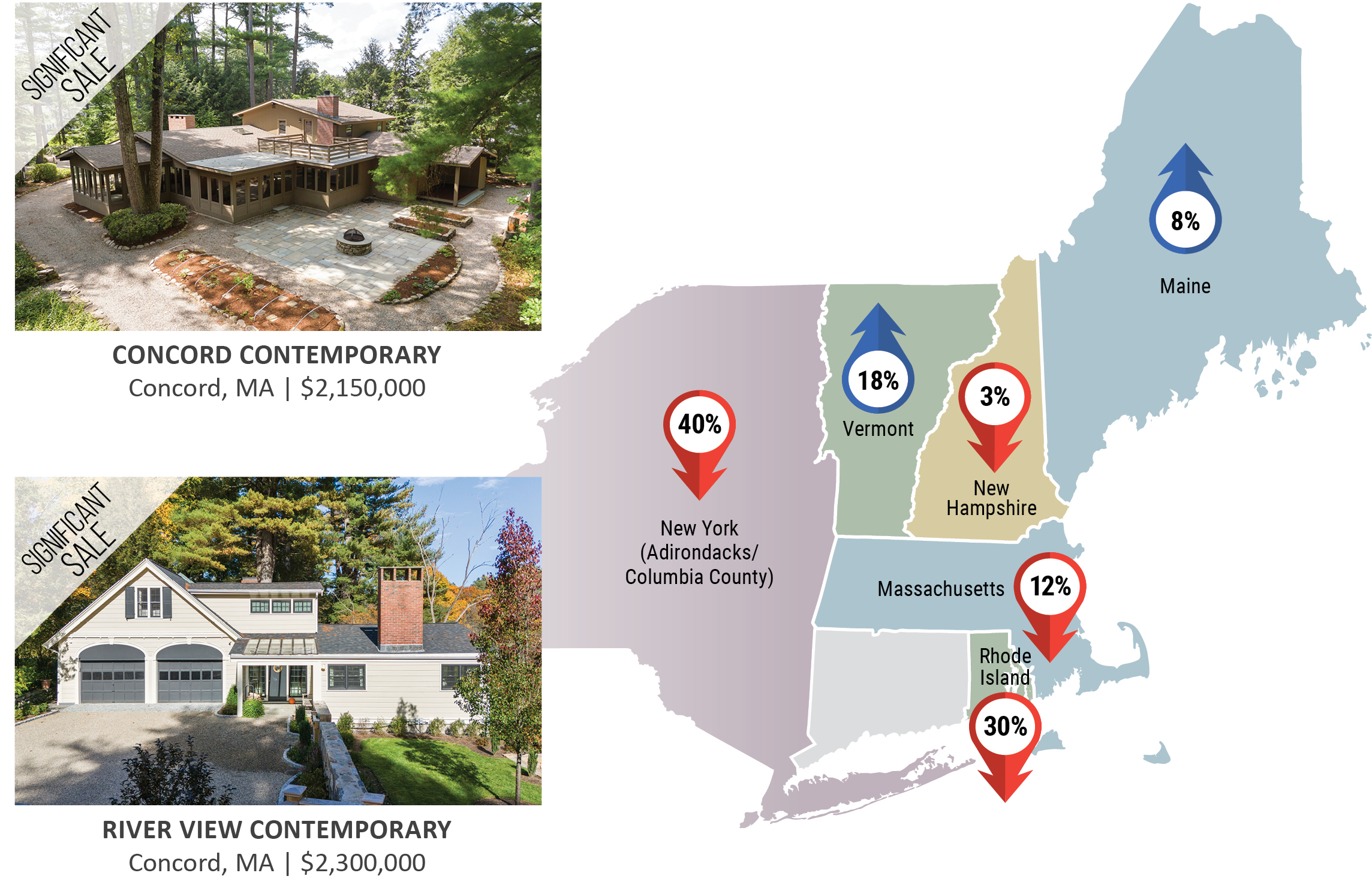

New England & The Adirondacks Markets

Young continues: Lack of inventory has been a problem since the emergence of COVID in 2020. While frustrating for buyers, sellers benefitted from multiple offers and the accompanying upward pressure on prices. Last year we observed that climate change was a motivating factor for buyers from the West Coast to move to New England. This year the cost of property insurance and even availability at any cost, muddied deals often emerging at or near closing.

Maine was the only state market with growth in high-end sales: +8%. In the other 5 states, sales decreased: Massachusetts: -12%, New Hampshire: -3%, New York (Adirondacks/Trilakes, Columbia and N.Dutchess counties): -40%, Rhode Island (Newport and Washington counties): -30%, and Vermont:-18%.

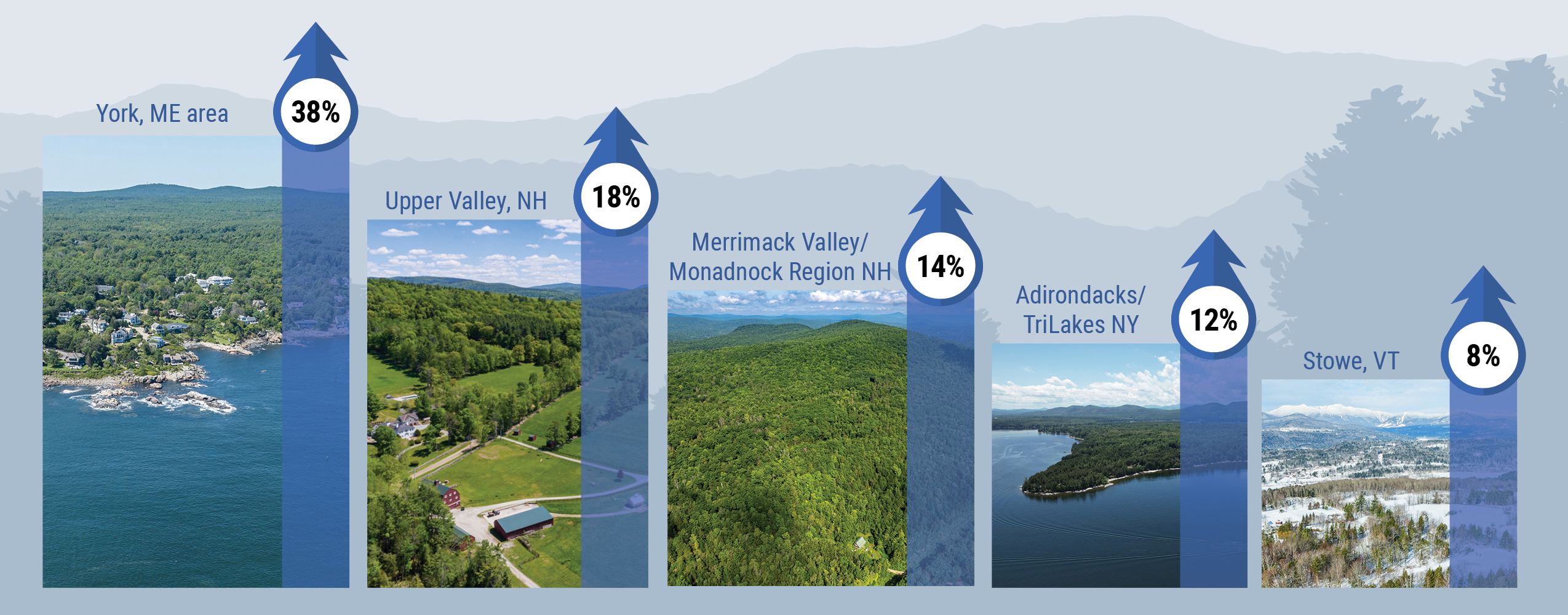

Within these state markets, 6 of the 32 markets making up the LandVest Index had increases in sales: York ME area: +38%, Upper Valley NH: +18%, Merrimack Valley/Monadnock Region NH: +14%, Adirondacks/TriLakes NY: +12%, Stowe VT: + 8%, and Lakes Region NH +3%. Within the other 26 markets, the smallest decreases in sales were all in MA: Berkshire County: -2%, West & Central (Franklin,Hampshire, Hampden counties): -3%, and Worcester County: -4%. The largest decreases in sales were in Columbia County NY (upper Hudson River Valley adjacent to the Berkshires in MA): -65%, Washington County RI: -42%, and Sunapee Region NH: -33%.

The three large vacation markets in Massachusetts slowed their growth in sales for the second year in a row after two years of exceptional COVID-driven increases: Cape Cod: -13% vs -7% in 2022 and +12% in 2021, Marthas Vineyard: - 19% vs -27% in 2022 and +26% in 2021, and Nantucket: -6% vs -43% in 2022 and +27% in 2021.

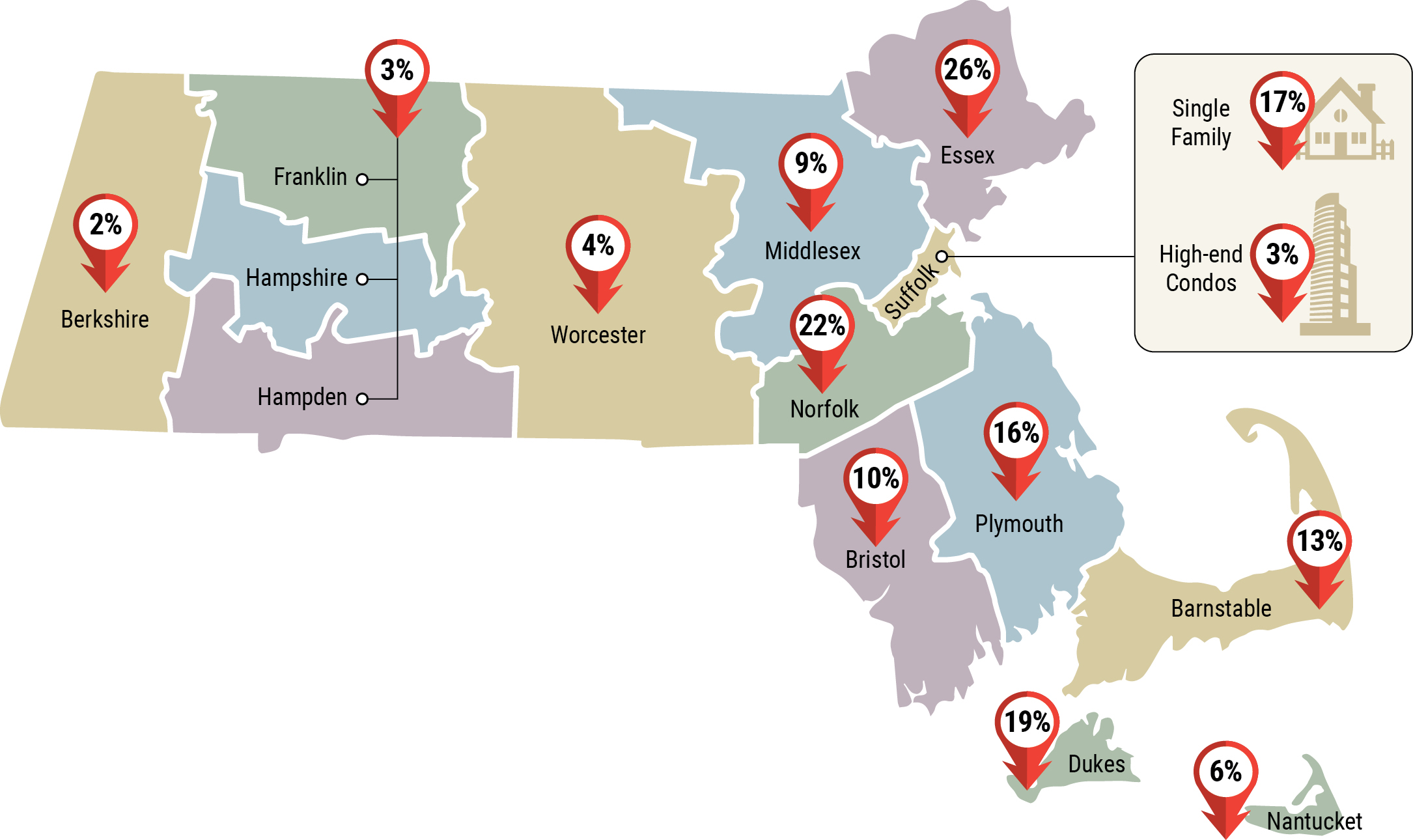

Massachusetts Market

In Massachusetts, sales were down in all markets. The smallest decreases were in Berkshire County: -2% vs +11% in 2022, West & Central MA (Franklin, Hampshire, and Hampden counties): -3% vs +36% in 2022, and Worcester County: -4% vs +52% in 2022. The largest decreases in sales were in Essex County -26% vs +9% in 2022, Norfolk County -22% vs +22% in 2022, and Dukes County (Marthas Vineyard and Gosnold): -19%.

Other Market Highlights

Rate relief and growing inventory is the theme heading into 2024. But until inventory recovers fully, it remains a sellers market in most of our key regions. If mortgage rates can get below 6% in 2024, then many sellers who were reluctant to part with their sub-3% mortgages, may now be willing to move, saidSlater Anderson, Managing Director of Real Estate at LandVest | Christies.

Inflationary pressures of 2023 led to higher material and labor costs and broader economic uncertainty. As these pressures have eased, there have been more buyers willing to take on renovation and new construction projects. At higher price points in our markets, cash buyers remain mostly unaffected by elevated interest rates. As a result of these factors, we see a moderate rebound in home sales volume in 2024 with the luxury market pricing remaining strong.

The LandVest Real Estate Index is a periodic review of select high-end markets in Maine, Massachusetts, New Hampshire, Vermont, and the Adirondacks. Market data are collected from Multiple Listing Services anddo not include private listings. LandVest makes no representation as to the accuracy of the data and therefore is not responsible for any actions taken as a result of use of or reliance on this information.

The New England Luxury Real Estate Report is an annual review of select high-end markets in Maine, Massachusetts, New Hampshire, Rhode Island, Vermont, and the Adirondacks. Commentary and insights are provided by Luxury Real Estate Advisor [...]

The economy feels unsettled. Unemployment is negatively impacting white collar jobs. Consumer sentiment is down. The Federal Reserve is holding rates flat, with no clear timeline for cuts. Costs remain high, and uncertainty is a constant in conversation.

LandVest | Christie’s International Real Estate closed more than $1 billion in residential sales in 2025. The result reflects a year of disciplined growth across New England, with an average sale price of $2.5 Million

To landvest.com

To landvest.com

Follow Us on Social Media